The Quit Number: How Much Money You Actually Need Before You Can Safely Quit

Most people guess when it comes to the finances of quitting. Here's how to calculate the actual number - and why most people get it wrong.

Most people decide to quit based on a feeling. The money stuff gets figured out later, or estimated loosely, or thought about with more optimism than accuracy.

This is usually where it goes wrong.

Not the decision to leave - that part might be completely right. But the financial preparation around it is where people underestimate what they need, leave before they’re ready, and end up making their next career move under financial pressure instead of from a position of choice.

Here’s how to actually calculate the number.

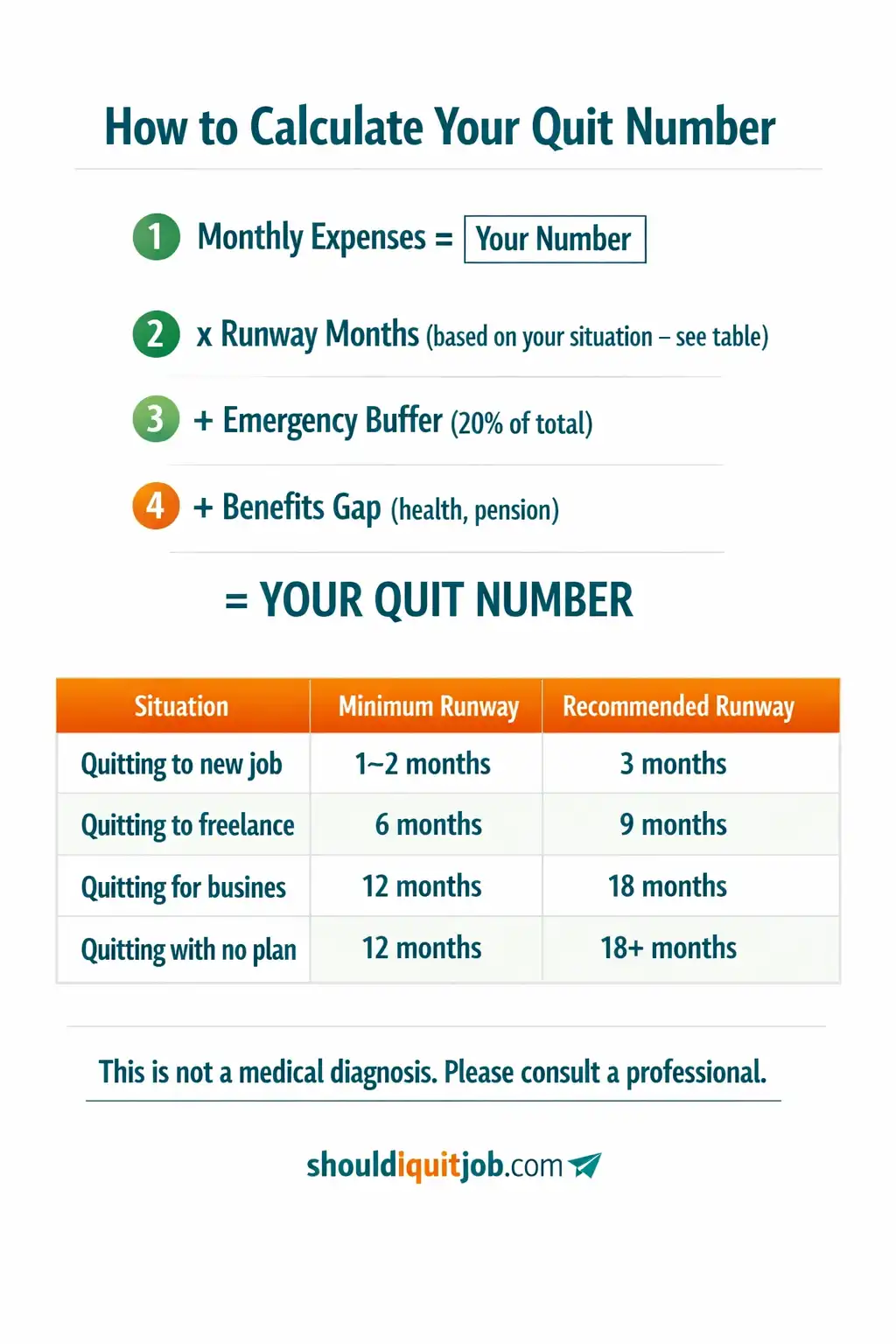

The Basic Formula

Your quit number is the total savings you need before leaving your job safely.

It has three components.

Monthly expenses × runway months. Take everything you spend each month - rent or mortgage, food, bills, transport, subscriptions, debt repayments, everything - and multiply by how many months you’d need before income resumes. That’s your base.

Benefits replacement. This is what most people forget. When you’re employed, your employer covers costs you don’t see: pension contributions, health insurance (where applicable), possibly a travel allowance, life insurance, professional memberships. When you leave, those costs either disappear or land on you. For most people in salaried employment this adds 15 to 25 percent to your effective monthly cost.

Emergency buffer. Add 20 percent on top of everything. Because searches take longer than expected. Because a freelance client takes three months to pay. Because an unexpected cost arrives at the worst moment. The buffer isn’t pessimism - it’s what makes the plan survivable when reality diverges from the projection.

Quit number = (monthly expenses + benefits replacement cost) × runway months × 1.2

What “Runway” Actually Means

Runway is the number of months you’d realistically need between leaving and receiving regular income again.

Most people underestimate this, for two reasons. They’re optimistic about how quickly they’ll land something. And they’re thinking about the best case - the job that comes through in week three - rather than a realistic central estimate.

Here’s a more honest breakdown by situation.

| Your next step | Minimum runway | Recommended |

|---|---|---|

| New job already accepted before leaving | 1 month | 3 months |

| Job searching after leaving | 3 months | 6 months |

| Freelancing or consulting | 6 months | 9 months |

| Starting a business | 12 months | 18 months |

| No plan yet | 12 months | 18+ months |

The minimum is the floor - what you’d need if everything goes well. The recommended is what gives you room to breathe, to be selective, and to survive the things that don’t go to plan.

The Benefits Gap Most People Miss

If your employer provides health insurance and you’re in the US, this is the biggest single variable. COBRA continuation coverage typically runs $500 to $800 per month for an individual - costs you weren’t paying while employed. Budget for this from day one.

In the UK, NHS coverage continues regardless of employment, but employer pension contributions stop. If your employer was matching 5 percent of your salary, that’s income you were effectively receiving that disappears the moment you leave. Calculate the monthly value and add it to your expenses.

Other common gaps: death-in-service insurance, income protection, dental/optical cover, season ticket loans that need repaying. Run through your benefits statement and convert each item to a monthly cost. The total is often surprising.

The Five Scenarios That Drain Runway Differently

Your runway number assumes things go reasonably to plan. Here’s what each major deviation looks like.

Scenario 1: Job search takes twice as long as expected. The average job search for a professional role runs 3 to 6 months. If yours takes 9, and you budgeted for 6, that’s 3 months of additional spend against your savings. The 20 percent buffer is specifically designed to absorb this.

Scenario 2: Freelancing starts slowly. The first paying client rarely arrives in week one. Most freelancers see their first reliable income after 2 to 4 months. If you’ve budgeted based on “I’ll start billing clients immediately,” the gap before that happens will eat through your runway faster than you projected.

Scenario 3: Business takes longer to generate revenue. Statistically, most businesses take 12 to 24 months to reach financial sustainability. Building a runway on the assumption that yours will be faster is a risk.

Scenario 4: Unexpected personal expense. Car repair, emergency travel, medical cost. Without a job to absorb it, a single unexpected £2,000 expense becomes a meaningful hit to your runway.

Scenario 5: You discover you hate your next thing too. This happens more often than people plan for. You leave, start the job search, realise you don’t want another job in the same field, and need more time to figure out what comes next. Extra months of clarity-seeking eat runway.

The buffer handles most of these. But building your runway to the recommended figure rather than the minimum is the real protection.

A Worked Example

Let’s use a concrete set of numbers.

Monthly expenses: £2,500 Benefits replacement (pension, insurance): £300/month additional Adjusted monthly burn: £2,800

Situation: Quitting to job search, no role lined up. Recommended runway: 6 months.

Base calculation: £2,800 × 6 = £16,800 Add 20% buffer: £16,800 × 1.2 = £20,160

That’s the quit number. Not a guess - the specific amount you need in savings before leaving is genuinely lower-risk.

If the same person were planning to freelance, the recommended runway becomes 9 months. £2,800 × 9 = £25,200 × 1.2 = £30,240

And if starting a business: £2,800 × 18 = £50,400 × 1.2 = £60,480

The numbers are different depending on what you’re doing next. Which is why “how much do I need to quit?” can’t be answered without knowing the answer to “and then what?”

What If You’re Not There Yet?

Most people who calculate this number realise they’re short - see should I quit without another job lined up. That’s not a reason to give up - it’s a reason to build a plan.

The 90-day sprint. Work out the gap between what you have and your quit number. Now divide by three. That’s your monthly savings target for the next quarter. What would have to change for you to hit that? Expenses to cut, income to add, assets to liquidate?

Quiet job searching while employed. The best time to find your next job is while you still have one. You’re not desperate. You can be selective. You have leverage in salary negotiations. Start the search before you have a pressing reason to, and your exit happens from a position of strength rather than urgency.

Medical leave as a bridge. If your reasons for leaving include your health, medical leave can provide income continuity while you build the runway. It’s not a way to game the system - it’s using the protection that exists for situations exactly like this.

One more year, intentionally. If you’re not close to your quit number, a year of deliberate saving - with a specific target and a committed exit date - is often the right call. Not staying indefinitely. Staying with a plan and a deadline.

The point of calculating your quit number isn’t to build obstacles. It’s to make the decision clearly.

Once you know the number, you know two things: whether you’re ready to go now, or how far you are from being ready. Both are useful. Both are better than guessing.

Ready for your answer?

Get a data-backed verdict in 2 minutes

13 questions. Personalised Leap / Wait / Stay verdict. Financial runway analysis. Basic report free · Full analysis available · No login required.

Analyse My SituationThis content is for informational purposes only and does not constitute professional financial, career, or psychological advice. If you're experiencing symptoms of depression, anxiety, or burnout, please speak with a qualified health professional.